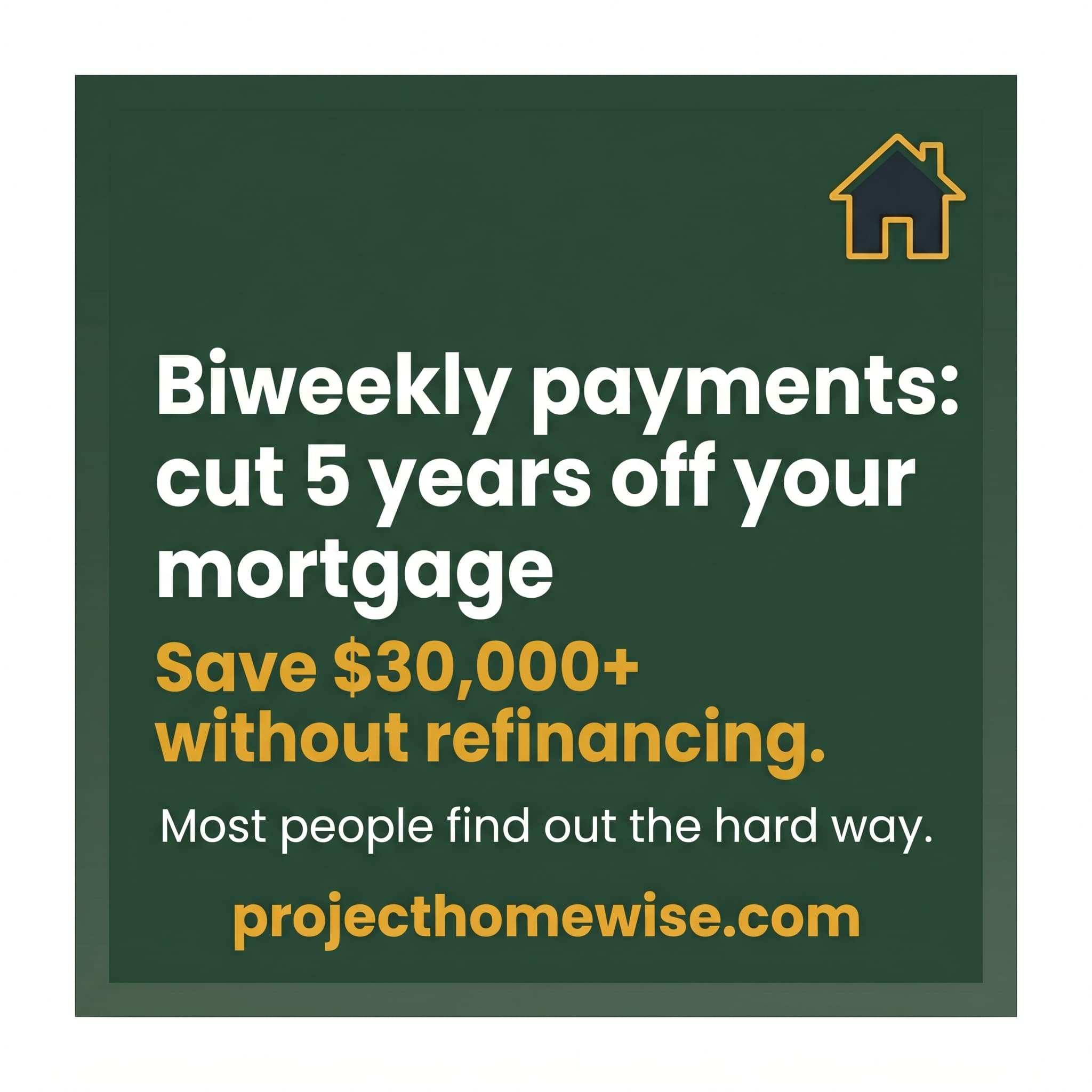

On a $350,000 mortgage at 7%, switching to biweekly payments instead of monthly ones saves you roughly $47,000 in interest and cuts about five years off your loan — without changing anything else about your rate or terms.

How Biweekly Payments Actually Work

Monthly payments mean 12 payments a year. Biweekly payments mean one payment every two weeks, which adds up to 26 half-payments — or 13 full payments — annually. That one extra payment goes directly toward your principal balance.

Because your loan balance is slightly lower every time interest is calculated, less of each subsequent payment goes to interest and more goes to principal. This effect compounds over time. The savings are not from the timing itself — they come from that one extra principal payment each year eating down the balance faster than the amortization schedule assumed.

On a 30-year, $350,000 loan at 7%, the math looks like this: your standard monthly payment is about $2,329. Over 30 years you pay roughly $488,000 in interest. With biweekly payments, you pay off the loan in about 25 years and 3 months and pay about $441,000 in interest. The difference is $47,000 and nearly five years of payments you never have to make.

The Setup Trap Most Homeowners Fall Into

Here is where the lender part matters. Many lenders offer a “biweekly payment program” — often for a setup fee of $200–$400. Some charge ongoing monthly fees to manage it. What you are actually paying for is the lender holding your biweekly payment for two weeks and then applying it as a full monthly payment, which accomplishes nothing.

You do not need to enroll in any program. You can replicate the exact same effect on your own for free. Divide your monthly payment by 12 and add that amount to your regular monthly payment, earmarked as extra principal. Or just make one full extra principal payment once a year, manually. The result is mathematically identical to biweekly payments.

If you do want to pay biweekly, confirm with your servicer that they will apply the half-payment immediately to your account and not hold it until the second payment arrives. If they hold it, the interest-reduction benefit disappears entirely.

When Biweekly Payments Make the Most Sense

The biggest gains come early in a 30-year loan. Interest front-loading means a larger share of your early payments goes to interest rather than principal. An extra principal payment in year three has more impact than the same payment in year twenty-two, because it prevents decades of compounding interest on that balance.

This strategy works best when your mortgage rate is meaningfully higher than what you could reliably earn in low-risk savings or investments. If your rate is 7% and a high-yield savings account is paying 5%, paying down the mortgage earns you a guaranteed 7% return — better than the savings account and with no risk. If your rate is 3% and you can invest at higher returns, the math may favor investing the extra payment instead.

It also depends on your cash flow. Before committing to biweekly payments, make sure you have a solid emergency fund in place. Accelerating your mortgage payoff at the cost of liquidity creates a different kind of risk.

How to Set It Up Without Paying Anyone

Call or log into your servicer’s portal and confirm you can designate extra payments as “principal only.” Most major servicers allow this online. Then pick one of two approaches:

Divide your monthly payment by 12. Add that amount to your regular payment each month as extra principal. For a $2,329 payment, that is roughly $194 extra per month — which totals one full extra payment per year.

Or simply mark your calendar for one month a year and make a full extra principal payment. January or July works well since those months are not aligned with major annual expenses.

The key step either way: confirm your servicer is applying the extra amount to principal and not to your next month’s payment. A misapplied extra payment does nothing for your balance. Check your statement after the first payment to verify the principal balance dropped by the expected amount.

Questions Homeowners Ask

- When does refinancing actually make financial sense?

- How do you get rid of PMI and how much does it save?

Compare Mortgage Options Today

See current rates and find a loan that gives you the flexibility to pay it down on your terms.

View Mortgage Rates →

Leave a Reply